Let Florida Be A Lesson, Not A Loss: A Warning for the National Housing Market

- Responsible Alpha

- Apr 7

- 2 min read

As rising sea levels and repeated storms become the new normal in Florida, the state is confronting a silent financial disaster. What began as an environmental threat has evolved into a deep systemic crisis affecting insurance, mortgages, and the stability of entire communities. The climate crisis in Florida is no longer just about stronger hurricanes or hotter summers—it’s about the unraveling of homeownership, investor confidence, and public trust in financial systems.

Why This Matters

Insurance Industry Collapse: Thousands of claims go unpaid as smaller insurers declare bankruptcy following each big storm. Residents in vulnerable areas are confronted with high and unpredictable premiums as major carriers pull out of the market.

Taxpayer Exposure through GSEs: Mortgages linked to hazardous insurers are still backed by government-sponsored enterprises (GSEs) such as Fannie Mae and Freddie Mac. The federal government and taxpayers are in danger of another financial collapse as a result of these decisions.

Unchecked Development and Hidden Costs: Houses in flood-prone areas are being sold, insured, and funded despite the growing dangers. Just between 2009 and 2018, Florida could have saved $95 billion in mortgage volume by implementing risk pricing and modernizing its regulations.

Details

The increasing severity of climate change is putting a strain on Florida's housing and insurance markets:

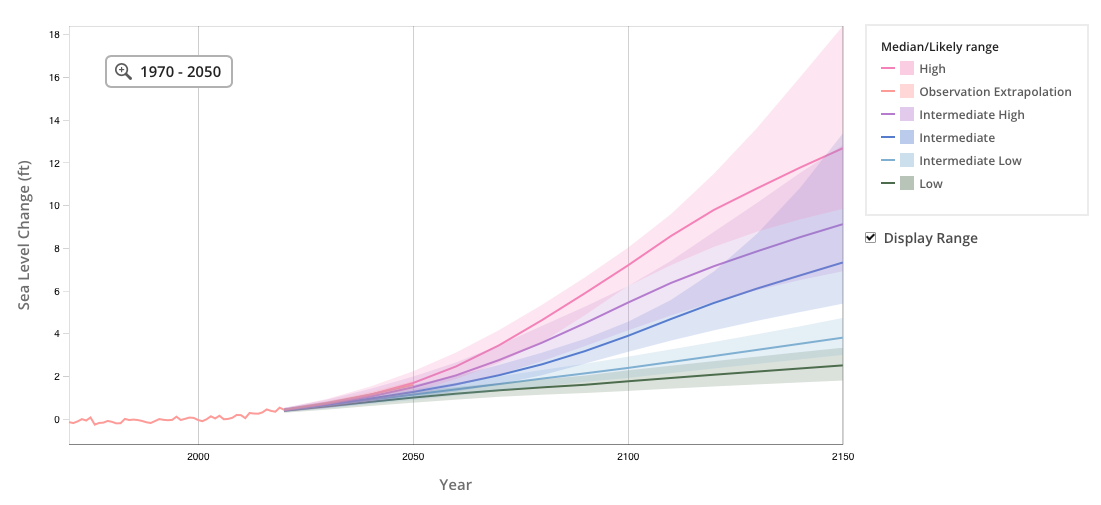

Sea Level Rise (SLR): Damage from flooding, storm surge, and saltwater intrusion is accelerating the degradation of coastal infrastructure. Transportation delays, hospital closures, and power outages are starting to feel like the norm.

Investor Hesitancy: Those who prioritize environmental, social, and governance (ESG) issues are avoiding the riskiest regions. Major market players persist in disregarding the fundamental climate risks, despite disclosure laws mandating transparency.

Mortgage and Market Risk: Houses that have been flooded lose value, the default rate goes up, and properties that do not have enough insurance are not allowed to get loans. Once again, these are the precursors to the housing crisis of 2008; however, this time, climate change, rather than credit, is at the heart of the problem.

Action Items

Build long-term resilience and lessen the impact of a complete market collapse by doing the following:

Connect Insurer Quality to Mortgage Eligibility: The federal government should not support loans that are underwritten by risky insurers. Demotech and similar agencies need to be subjected to more stringent regulations.

Update Rating Agency Frameworks: Climate change, rising sea levels, and severe weather events should be included in mortgage risk models alongside creditworthiness and property value.

Center Resilience in ESG Policy: Sustainability, equity, and governance (ESG) models should prioritize climate-related monetary risk. Future investments should be driven by equity and resilience, not merely by emissions reductions.

Final Thought

Other coastal regions can learn from Florida's crisis. Reliving the past with even greater stakes awaits us unless we take immediate action to reform insurance, enforce transparency, and halt irresponsible development.

Let Florida be a lesson, not a loss.

Comments